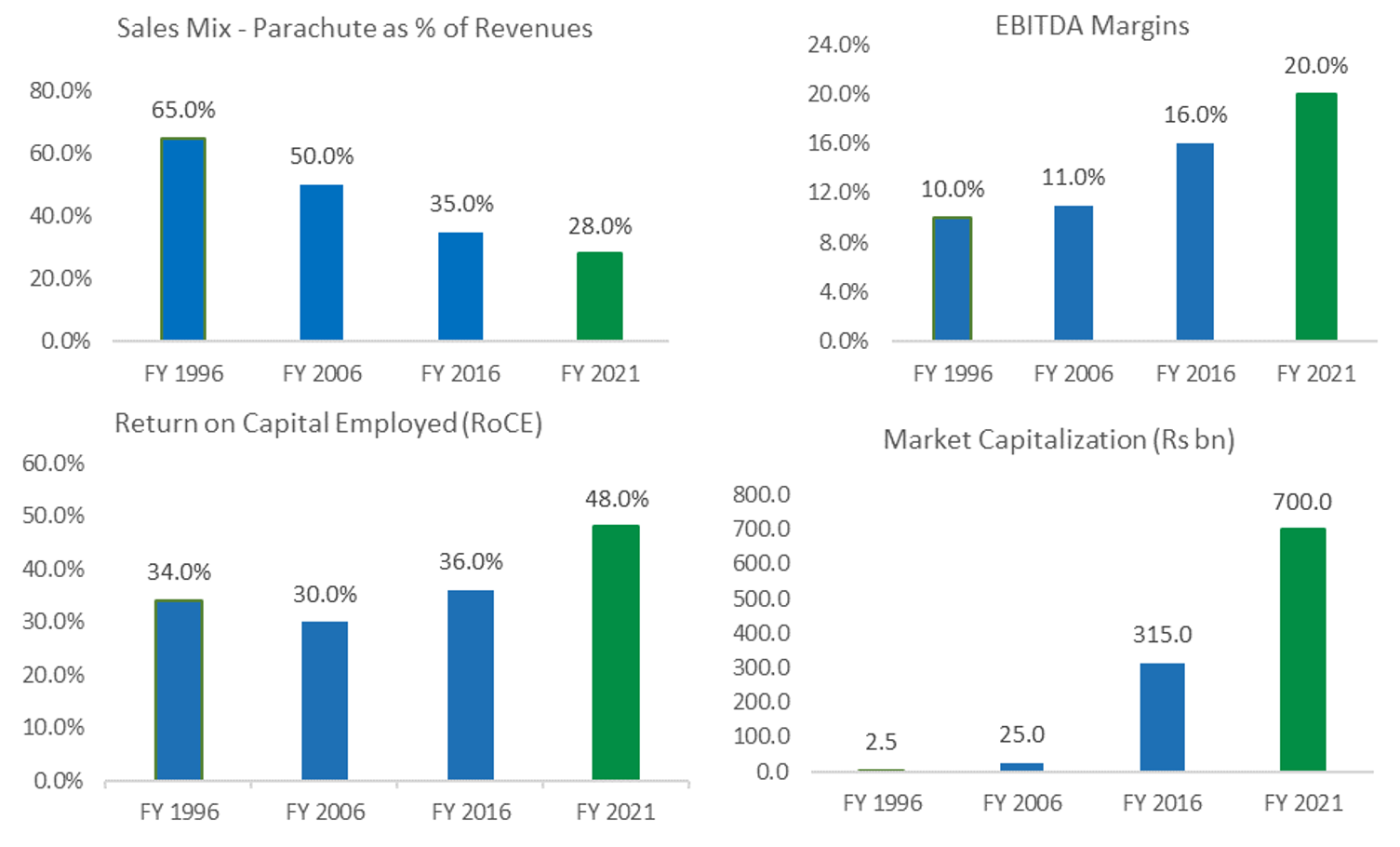

During the last 25 years, Marico has been able to compound revenues and profits at 13% & 18% respectively. It has achieved this through organic growth and a few strategic acquisitions. As a result, Parachute now contributes a quarter of consolidated revenues and its international businesses accounts for another quarter. During this period the company has faced raw material (copra) inflation challenges on multiple occasions and done well to protect the franchise and profitability. Operating profit margins have been consistent and have improved particularly in the last few years.

Marico has also strategically acquired brands in India and Asia to further broad base its revenue composition. The acquisition of ‘Nihar’, a coconut oil brand from a strong competitor like Hindustan Unilever was the seminal moment for the company. Post this the company was able to consolidate and establish a dominant position in the coconut oil market. Additionally, it has also acquired brands from Reckitt Benckiser in India and few other brands in Malaysia and Vietnam.

Over the last 25 years Marico has grown, diversified it revenue and profit base, improved its margins and profitability. Its amongst the few Indian consumers companies who have succeeded at growing and scaling its business over the last 20-25 years and consistently delivered solid operating performance. Investors have recognized its strength which has resulted in its market capitalization going up 275x since its IPO having compounded at 26% CAGR.

The company now trades at its lifetime high price and the valuation discount to MNCs has narrowed considerably. A question that comes up regularly is why we still own Marico in our portfolio at this juncture and what do we expect.

We like the company for:

- Its competitive positioning in the core business of hair and edible oils

- How it is building out its foods and international businesses

- Its attempt to build a new growth engine via D2C/new age brands

Marico has a strong core business (50% of consolidated revenues) comprising its Parachute and Value-added hair oils franchise in India. Parachute is a strong and well entrenched brand with a 50%+ market share. It has an extraordinarily strong sourcing advantage which positions it well to convert loose oil users and grow the business. The company is a leader in value added hair oils which has been growing steadily at 10-15% over the last 10 years barring the last couple of years. We expect this portion of its business to compound at 9-10% in value terms.

Saffola oil and foods business (20% of consolidated revenues) has done well over the last few years. The edible oil business got a boost from the Covid 19 pandemic as lock downs and work from home meant increased home cooking. Savory oats launched a few years ago have done very well and has resulted in category creation. On that success, Marico has recently entered other foods categories viz. honey, noodles, protein nuggets building on the strong health equity of the Saffola brand. We like these initiatives to drive innovation and growth in this franchise. Overall, we expect the oils and foods side of the business to grow 25% annually over the next 3-5 years.

International businesses across Asia and Africa account for a quarter of revenues off which Bangladesh is fifty percent. Marico is replicating the India playbook in Bangladesh with leadership position in coconut oil. With non-coconut oil business having grown rapidly in the last 5-7 years, it already accounts for half the business. Vietnam is another operation where the company has a strong market position in male grooming category and is building on this strength to drive growth. Overall, we expect the international operations to grow 10-12% annually.

Covid 19 has hastened the adoption of online commerce. Growth and reach of platforms like Amazon and Flipkart and adoption and maturity of digital marketing and communication has lowered the barriers to entry for smaller and startup consumer brands. Such companies are now able to launch differentiated products across an entire range of categories (existing and emerging) with focused yet limited communication budgets to create brands and reach consumers directly (D2C). Outsourced production and go to market allow these new companies to choose their battle grounds and rapidly scale with success. These D2C brands are attempting to enter large existing and niche categories with differentiated products to take advantage of the evolving consumer preferences.

Marico is attempting to leverage on these changes taking place and build an additional growth engine by entering new categories through a combination of in-house and acquired brands. We read Marico’s D2C strategy as serving the dual purpose of defending its core franchise as well as enabling it to expand its addressable market with new products. The company acquired “Beardo”, a male grooming brand a few years ago. In addition, it has launched its own D2C brands “Pure Sense” and “Coco Soul” and very recently acquired a majority ownership in a beauty care brand “Just Herbs”. Marico, through these initiatives will enter large personal care categories such as skin and hair care. As an example, an Indian herb-based shampoo/skin cream helps them set the ground differently vs. launching a shampoo with limited product differentiation and equity. If Marico scales these brands over 5 years to about 5%+ of overall revenues, this would add 2-3% to its expected growth rate.

We think Marico is very well placed to take advantage of the ongoing changes and disruption in the consumer landscape. The strength of its core brands along with the cash flow it generates, permits Marico to experiment and try to build in adjacent emerging categories. We expect the company to compound revenues at low to mid-teens and profits a little ahead. However, profit growth could accelerate in the medium-term as newer engines of the group viz. foods and D2C brands gain size and contribute meaningfully to overall revenues. We remain believers in the management capability and the execution of Marico.

Market & Performance Update

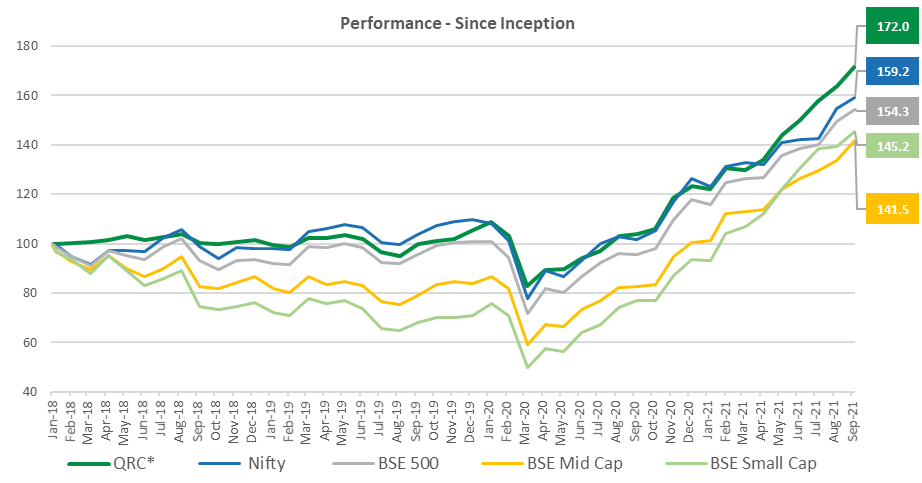

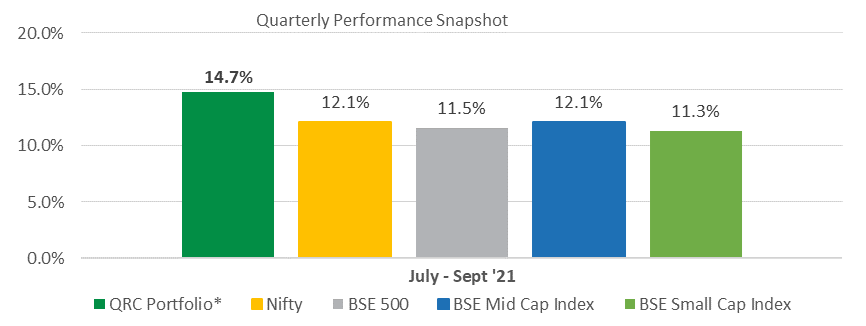

For the 1st Half of FY22 (April 2021 to September 2021), the QRC Long Term Opportunities Portfolio (LTOP) was up 32.5%. Our 1-year return for the period October 2020 to September 2021 period is 65.3%. Stock markets continued their broad-based rally during the last quarter driven by improving economic data and an encouraging commentary from companies on an improving demand scenario post the second wave of Covid. Signs of normalization and the continued interest from domestic and foreign investors has kept the equity markets well supported.