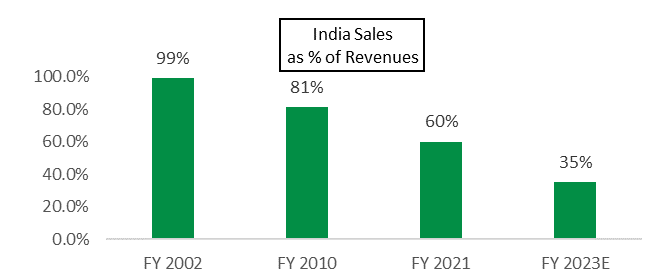

The last few years have been a very challenging period for the auto sector and consequently for the automotive part suppliers with respect to growth. India has seen various regulatory changes regarding insurance & emission norms and both India & the international markets suffered at the hands of the covid-19 pandemic. Despite these headwinds, SEL, helped by its push into new products and geographies has managed to compound its revenues and profits at 12% and 15% respectively over the last 5 years – at a rate significantly faster than the automotive sector.

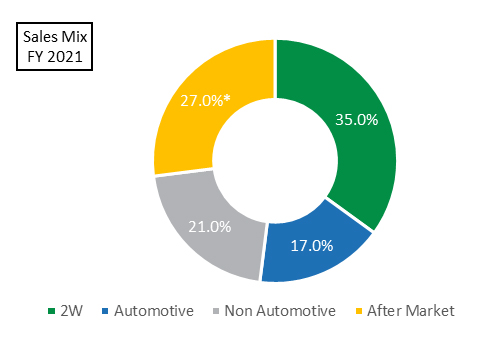

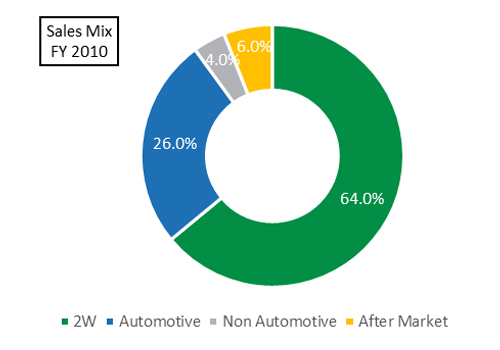

A higher share of lamps and international business in the mix has resulted in Operating margins (EBITDA) dropping marginally to 14-15% range from its earlier cables-only business margin range of 16-18%. However, business profitability (ROE) has remained steady in the ~20-22% range.

To push innovation and increase its share of wallet with its customers, Suprajit set up an R&D centre in Bangalore – Suprajit Technical Centre (STC) in 2015. The objective here was to improve value proposition for its cable customers and to develop new & technologically advanced products. Over the last few years, STC has filed 15 patents in products ranging from digital speedometer, throttle sensor etc. A speedier gear box with electromechanical clutches is in the final stage of commercialization. SEL has been able to win an estimated Rs. 1bn of additional business from some of these new products commercialized in STC.

In October 2021, SEL announced that it will acquire the Light Duty Cable (LDC) unit of Kongsberg Automotive at an enterprise value of US$ 42mn. This is a transformative acquisition for SEL, and it will emerge as a leading control cables player globally. This LDC unit supplies cable products to automotive, non-automotive and 2-wheeler segments and has a presence in the Electro-Mechanical Actuators (EMA) segment. SEL will acquire three plants in Mexico, Hungary, and China (Shanghai) where it has no existing manufacturing footprint. This business has marquee global customers such as Tesla, Honda, FCA, Land Rover, Lear Corporation, Magna amongst others in automotive, non-automotive and 2-wheeler businesses – a lot of these are new relationships for SEL.

With this acquisition, SEL also acquires the actuation technologies which it did not previously have, which it can offer to existing/other customers. LDC has certain unutilized capacities and in addition, there is head room to rationalize costs and overheads to improve margins of this business over time. Like its previous inorganic initiatives, SEL has been very disciplined with this acquisition. We believe this will have a pay-back of under 5 years and will add significant value to the company.

SEL now trades at its lifetime high. We continue to like the company for:

- Its strong presence in cables and lamps business globally and its effort to become a leading global cables manufacturer across geographies

- Its ability to do value accretive M&A

- Its ability to profitably grow revenue from existing customers through new products & geographic diversification

- Its ability to build a strong organisation with a stable and multi-cultural management team

Over the last 5-7 years (post the Phoenix lamps acquisition) SEL has been on its journey to transform from being a 2-Wheeler focused cables company operating in India to a diversified auto parts supplier across multiple products and geographies. Markets have appreciated its effort with the stock price up nearly 4x during this period. Currently the company trades at 18x its expected FY 23 earnings. We remain firm believers in the management and the execution capabilities of SEL. If this transformation journey and execution continues as in the past, we think Suprajit is very well placed to benefit from an impending auto cycle and grow and compound its share prices especially as it becomes more widely appreciated.

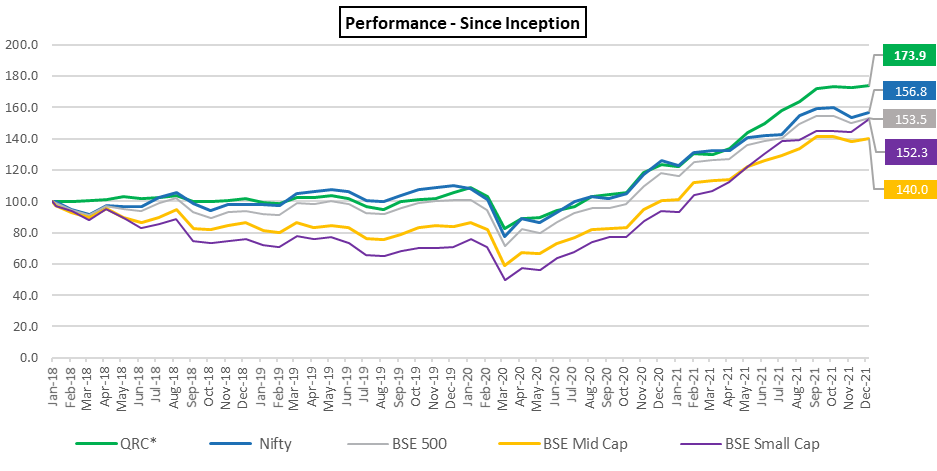

Market & Performance Update

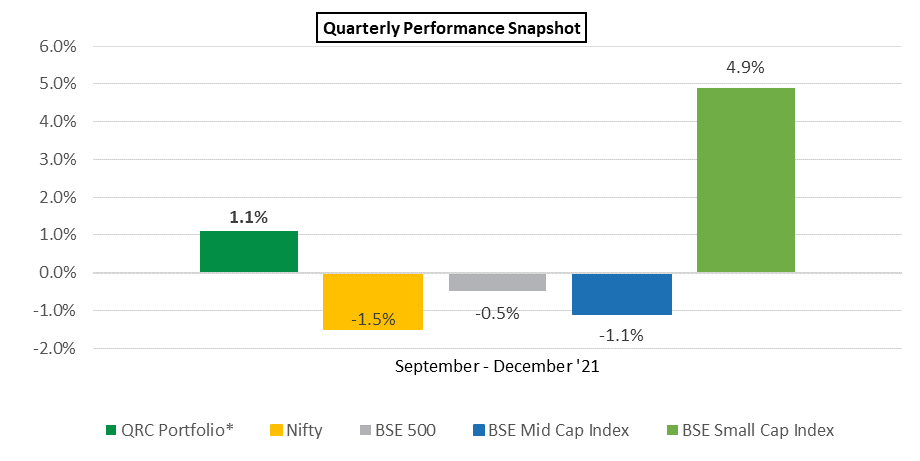

For the 9 months of FY22 (April 2021 to December 2021), the QRC Long Term Opportunities Portfolio (LTOP) was up 33.9%. Our 1-year return for the period January 2021 to December 2021 period is 41%. The broad-based rally seen during the last few quarters abated amid concerns of sharp rise in inflation (in India and globally) and worries around the spread of Omicron. The December quarter saw the benchmark Nifty index fall by 1.5% and the mid-cap index by 1.1%.