Dear Investor,

We hope this letter finds you and your loved ones safe and healthy.

Performance Update

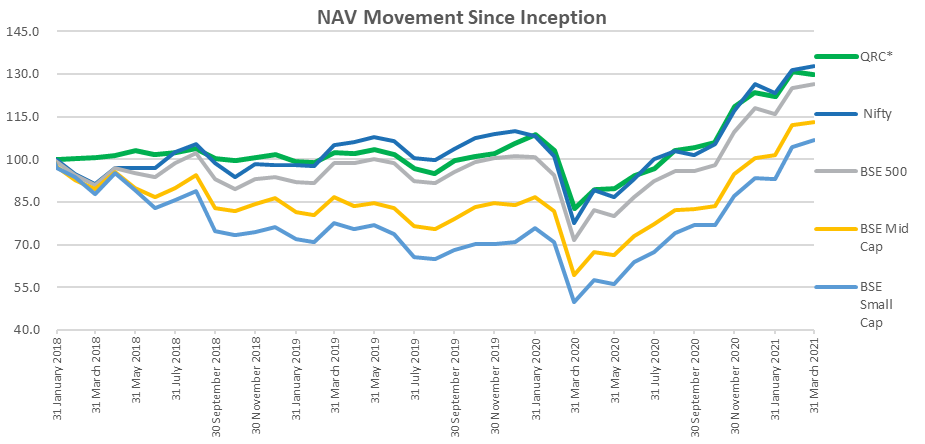

For the 2nd Half of FY21 (October 202 to March 2021), the QRC Long Term Opportunities Portfolio (LTOP) was up ~25% on top of the ~26% return delivered in the April to September 2020 period. Consistent and strong foreign flows and a hope and sense of normalcy and economic recovery aided the continued recovery in the broad markets post the covid-19 led slump in March 2020. Markets posted an all-round strong show in the last six months with small/mid cap companies, especially from the cyclical and beaten down sectors posting extraordinarily strong returns.

*Individual client portfolio returns may differ based on timing of their investment and specific instructions/circumstances. QRC returns are TWRR post fees & expenses. Source: BSE & NSE

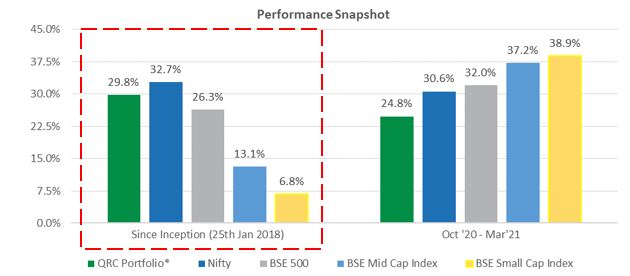

*Absolute returns. Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR. Source: BSE & NSE

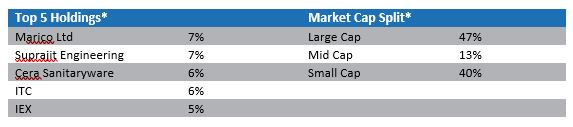

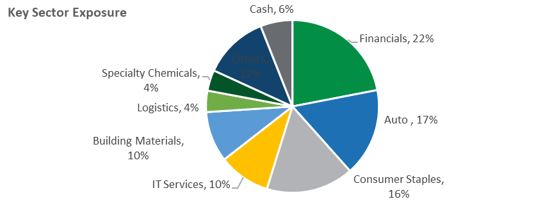

Portfolio Snapshot

*Illustrative. Individual client portfolios may differ based on timing of their investments and specific instructions/circumstances.

Why Quality?

Often, we are asked why we are so focused on owning Quality businesses and what this ‘Quality’ means. Quality, like beauty, lies in the eyes of the beholder. As we have said many times, Quality business for us needs to meet some basic criteria – should consistently earn a return on capital higher than cost of capital, should have a long runway for growth, should be self-funded (or have negligible debt) and should treat all stakeholders fairly. We will present this today with an example of a company that internally we put in the Quality Cyclical bucket i.e., one that we believe should help us play the economic growth but at the same time also help manage the downside in case this economic recovery remains elusive.

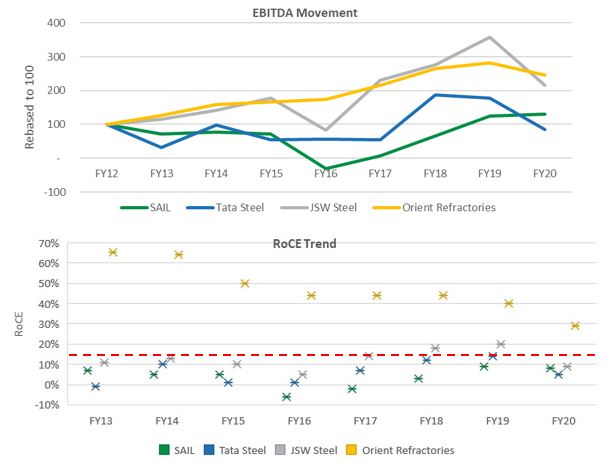

The company we are talking about is Orient Refractories (ORL). We have been building a position in this company in the portfolio since August 2018. Refractories are heat and pressure resistant material used for lining furnaces, kilns, reactors, and other vessels which hold and transport hot mediums such as metal and slag. ORL’s primary client base is steel manufacturers and hence ORL is an indirect play on the growth of the steel industry in India. Very simplistically, as the utilization and production in the steel industry grows, so does the use of ORL’s products and sales.

The question may then arise – if one is bullish on the steel industry, why not just buy steel companies? As the charts below demonstrate, for long periods of time, ORL has had a far stronger and steadier growth in EBITDA (operating profit) and has achieved this growth while being very highly productive with its capital. Another notable point is that that this growth has been entirely internally funded and unlike the steel manufacturers, ORL has not resorted to any external funding (debt or equity). A strong balance sheet ensures that when (not if) the downcycle returns to the steel industry, ORL will be in a far better position to manage the same.

To sum, supplying refractories is a far better business than steel manufacturing as seen by the higher RoCE as well as much lower swings in business fundamentals. While cycles will ebb and flow, the true ‘nature’ of the business does not change. We choose to invest in the better-quality business as that significantly reduces the burden of getting the cycle right.

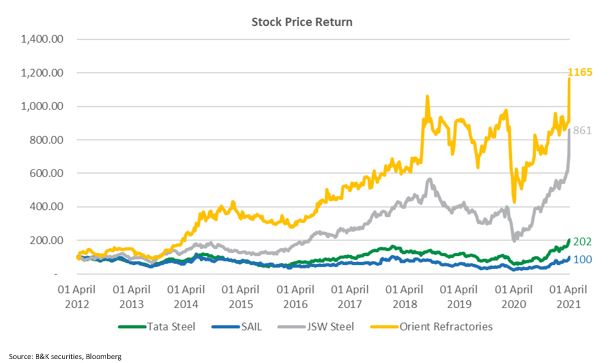

While in the short term this may seem like an overly conservative approach, the result of the strong fundamentals also translates into stock price performance (chart below) with far lower drawdowns and hence lower risk of bad investor behaviour.

Looking Ahead

The major highlight of the last few months was the Union Budget which was viewed by the markets as a positive in the absence of the highly feared higher taxes and fiscal conservatism. Instead, the govt. announced higher capex allocation and gave further impetus to the ‘Atmanirbhar’ Bharat / PLI scheme. For the time being, the RBI also continues to remain supportive with easy monetary policies. This macro backdrop remains constructive for equities as an asset class and small/mid cap stocks which tend to perform much better when the external environment is benign. We believe our exposure to financials, autos, building materials and logistics put us in a good position to capitalise on the impending revival in capex as well as growth recovery.

As we had mentioned in our previous letter, we think a large part of India Inc will report strong margins on the back of various cost cutting initiatives. Barring a wide-spread and uncontrolled second covid wave, we remain optimistic on earnings growth of our investee companies for the next 2 years and believe that we are at the beginning of a new economic cycle. As with previous growth cycles in India and emerging markets in general, the villain is often uncontrolled inflation – this is a risk that we will be tracking keenly and take appropriate portfolio action as and when required.

We thank you for entrusting us with your money. Do feel free to reach out to us with your questions or suggestions.

Sincerely,

Saurabh