Dear Investor,

The past few months have been a turbulent time for all market participants – investors and traders alike. The various Indian market indices are down

Stock Market Update

The year 2018 has been an eventful period to say the least with several developments that have caused significantly higher volatility in the Indian and global stock markets. From an Indian point of view, we have seen a key regulation change with the imposition of long-term capital gains tax on equity investments as well SEBI’s directive on re-classification of mutual fund schemes which resulted in significant turmoil in the stock market in the 1st quarter of calendar 2018.

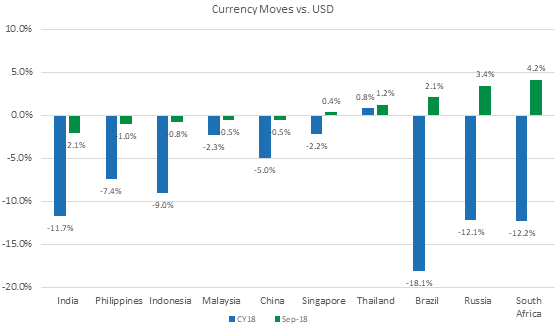

After nearly a decade of near zero percent interest rates, we have seen the US Federal Bank begin to raise interest rates as inflation starts to creep back into the economy and unemployment levels reach multi-decade lows. The rest of the developed world economies will likely follow on the path of slowing and eventually stopping their QE programmes and move towards tightening of interest rates. For us, higher interest rates in the developed world were a question of when and not if. A hitherto unforeseen development has been the protectionist policy stance taken by some of the major economies with USA renegotiating long-standing trade agreements and imposing multiple rounds of import duties on Chinese goods. These ‘trade wars’ also added to the macro worries in emerging economies and pushed the emerging market equities into ~9% correction in CY’18.

Rising global tensions and geopolitical worries have seen crude oil prices rise by 25% this year (to 4-year highs) and this along with a stronger US Dollar have raised concerns of deteriorating current account balances of major emerging markets reflecting in their currencies.

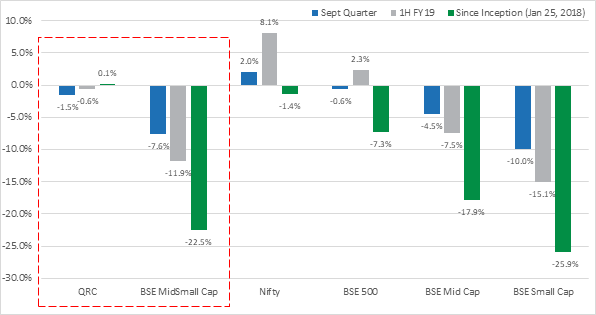

More recently, September saw the Indian markets sell-off sharply as NBFCs and some of the private sector banks were in the news for the wrong reasons. The default by IL&FS and the resultant tightness in the debt markets spread to equities too with the Nifty Bank Index falling by ~11% for the month. The widely tracked Nifty Index was down 6.4% but that belies the volatility and wealth erosion in the broader markets. The BSE500 index was down 8.8% and the smaller companies focused index like the BSE MidSmall Cap index lost 14.5%. The overall breadth of the market was also poor with advance decline ratio of 0.56 vs. average for the year at 0.80.

At QRC, we are comforted by the fact that despite the volatility and uncertainty caused by the above global and local factors, we have stuck to our philosophy of capital protection and selectively gone about building client portfolios. While we anticipated some of the macro headwinds, especially on the back of a very strong and narrow market performance since the 1st quarter of 2018, some of the global factors did catch us off-guard too. We are pleased to inform that in a very trying market, the QRC PMS portfolio has fared well and managed to outperform market indices.

*Individual client portfolio returns may differ based on timing of their investments and specific instructions/circumstances. QRC returns are TWRR.

QRC’s Investment Process

This is QRC’s first investor letter and we would like to spend some time highlighting and re-affirming our investment philosophy and process. This serves as a guiding post for all our investment decisions. As you know, we intend to run a market capitalization & benchmark agnostic investment strategy. In some of our small -cap stock, we are happy to assume a near-term liquidity risk for potential out-sized returns.

For us, the most important factor in a potential investment is that it is a Quality business – quality as understood by us to mean a business which consistently returns more than its cost of capital, has a healthy balance sheet, is run by an integral management team that has a track record of treating minority shareholders fairly and has grown and can continue to grow profitably at a faster rate than GDP for the foreseeable future. To identify these investment opportunities, we follow a thorough and in-depth Research process which entails building a detailed understanding on the key drivers of the business by discussions not only with key management personnel but also with competitors, suppliers and vendors of the investee company. At the core of our investment philosophy and what we hope will differentiate us over time, is our ability and willingness to Commit to an investment for the long-term (as defined by us to mean 3-5 years). We believe that with information asymmetry reducing significantly, an investor who can control his behavioural biases will stand out and have a higher probability of earning disproportionate gains.

We segregate our investment ideas in three main buckets. The first one is ‘Discovered Quality’ where we are happy to pay a high valuation for demonstrated growth and delivery by the business. These would be companies which are well-known by most investors. The second is ‘Quality in a Spot of Bother’ where an otherwise solid business is going through a period of slow growth/pain given external factors (e.g. higher crude prices or interest rates) or the company is embarking on an investment phase that may pressure near term earnings growth for a brighter future. The third bucket is ‘Emerging Quality’ where we think the business is demonstrating very good execution in an industry where they have competitive advantages that the market is yet to appreciate – the investment in this bucket will tend to be (but not necessarily) lesser known/smaller market capitalization companies.

We believe that in tough markets (and bear markets will follow bull markets just as night will follow day), it is the quality of the business and the depth of our research and understanding that will help us to avoid permanent loss of capital. We strongly believe in Warren Buffet’s words on investing – “Rule No. 1: Never lose money. Rule No. 2: Never forget rule No. 1.” This is the reason why we choose to invest in businesses with a proven track record of consistent and profitable growth and steer clear from deep turnaround plays or companies in highly cyclical sectors. A conservative approach that protects downside and steadily grows wealth is a better outcome in our view vs. one that ‘promises’ big returns but comes with significantly higher risks which are rarely, if at all ever fully understood. “To Finish first, you must first finish”.

Looking Ahead

We are not despaired with the on-going correction in the market prices from what were lofty valuations. The turbulence from the financial sector could spread till we see decisive action from the regulators and the government. We are also weary of the inflationary impact of a higher cost of energy and money (interest rates) on corporate earnings as well as the current and fiscal deficits. In addition, the markets may get worried about the upcoming central elections in 2019. We think these factors may present interesting buying opportunities. We are hopeful that over the next few months, we would have invested incremental capital in high quality businesses at prices within our comfort zone. We will continue to remain diligent and tight-fisted in deploying further capital.

We have tried to cover as many points that we felt might be of interest to you. If you have any questions or suggestions, we would love to hear from you.

Sincerely,

Team QRC